No investment recommendation. Make your own research and valuation before investing.

It is a discount retailer from the UK, founded in 1978. It has 777 stores in the UK and 135 stores in France. Additionally, it owns the store brand Heron Foods (frozen food), with 335 stores in the UK.

Their branded products consist of FMCG (Fast-Moving Consumer Goods) brands at competitive prices. Additionally, a big part of each store contains general merchandise products (GM), and some stores have garden products.

It does not have its own white label brand like Lidl and does not contain fresh products like vegetables or fruits. This makes me think that the company is more similar to Dollar Tree (and of course, B&M has similar margins…) than to Lidl.

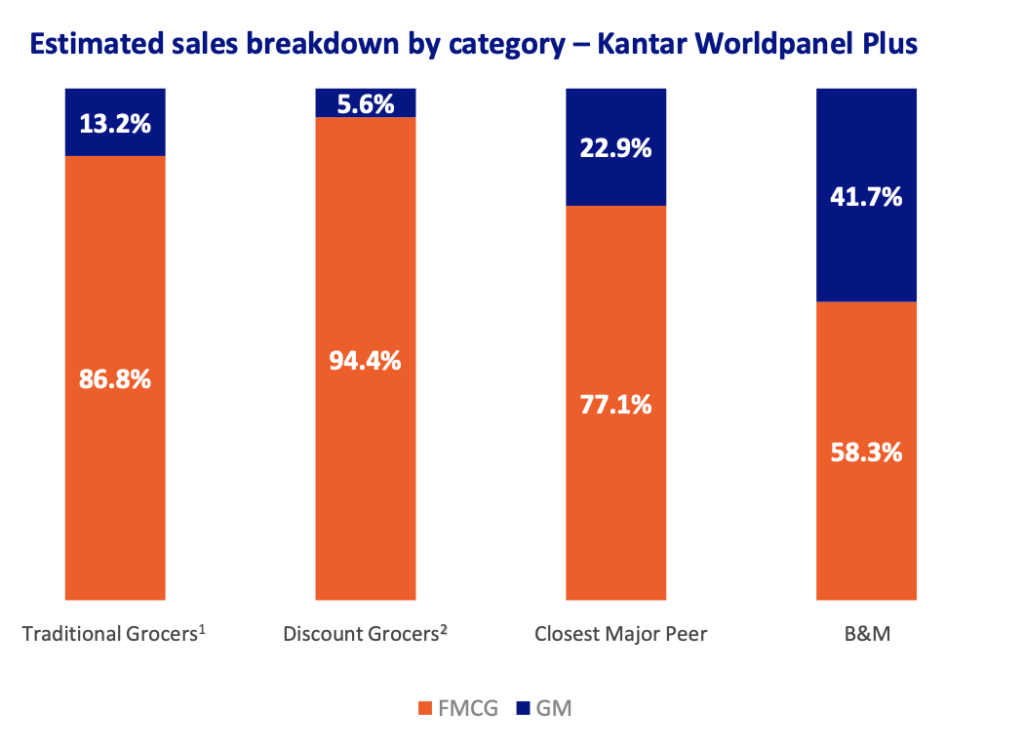

As we can see, the GM level of purchases over total is 41%, which is a key differentiation compared to competitors:

I am sure this helps to make the supply chain more efficient and reduces operational costs, improving margins. It avoids refrigeration, avoids a lot of waste, and has high-rotation products.

Numbers

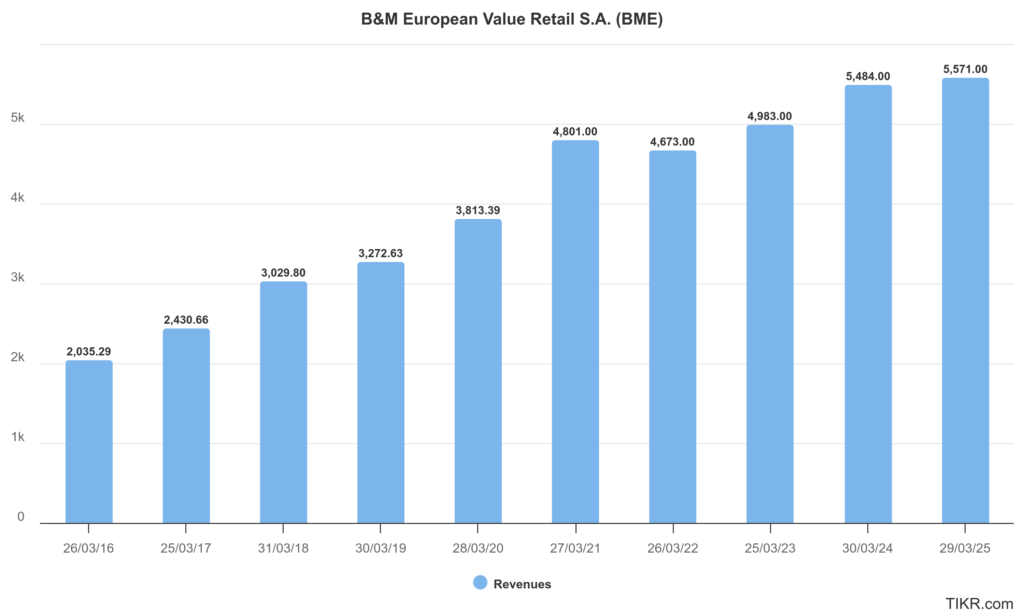

The company grew almost every year at a rate higher than 15% before 2022. After that, it had a decline of 2.7%, then back to growth of +6%, except last year when it only grew 1.6%, including a negative LFL in the UK.

It is important to note that I am using 53-week numbers to simplify comparisons, as is common practice in the retail sector due to weekly and seasonal variations. The company’s fiscal year ends in March of each year. That means, for example, that the 2021 revenue growth corresponds to panic buying during the pandemic. In 2022, we see a decline due to the unsustainable level of purchasing achieved the previous year.

The numbers presented for fiscal year 2025 look interesting and are the cause of the market stock decline. This decline put the company’s stock price at the same level as in 2016, when the company was at 37% (in EPS) of the current level… Okay, we can assume that at that time, the company was new in the stock market. The discount retailer in the UK was a relatively new concept, so it looked more like a growth company than a mature company like it does now. But I still think this is not a mature company as we understand it. It is not in decline; the company is still expanding its operations in two countries. So, valuing this company as a declining company at this time, I think, is not reasonable.

Back to the 2025 numbers, we see a mediocre growth level of 1.7% (below inflation) if we compare 53 weeks vs. 53 weeks. Of course, it is important to note that for 52 weeks vs. 52 weeks, the revenue growth is 3.7%, and the 53rd week contributes a negative -112 million.

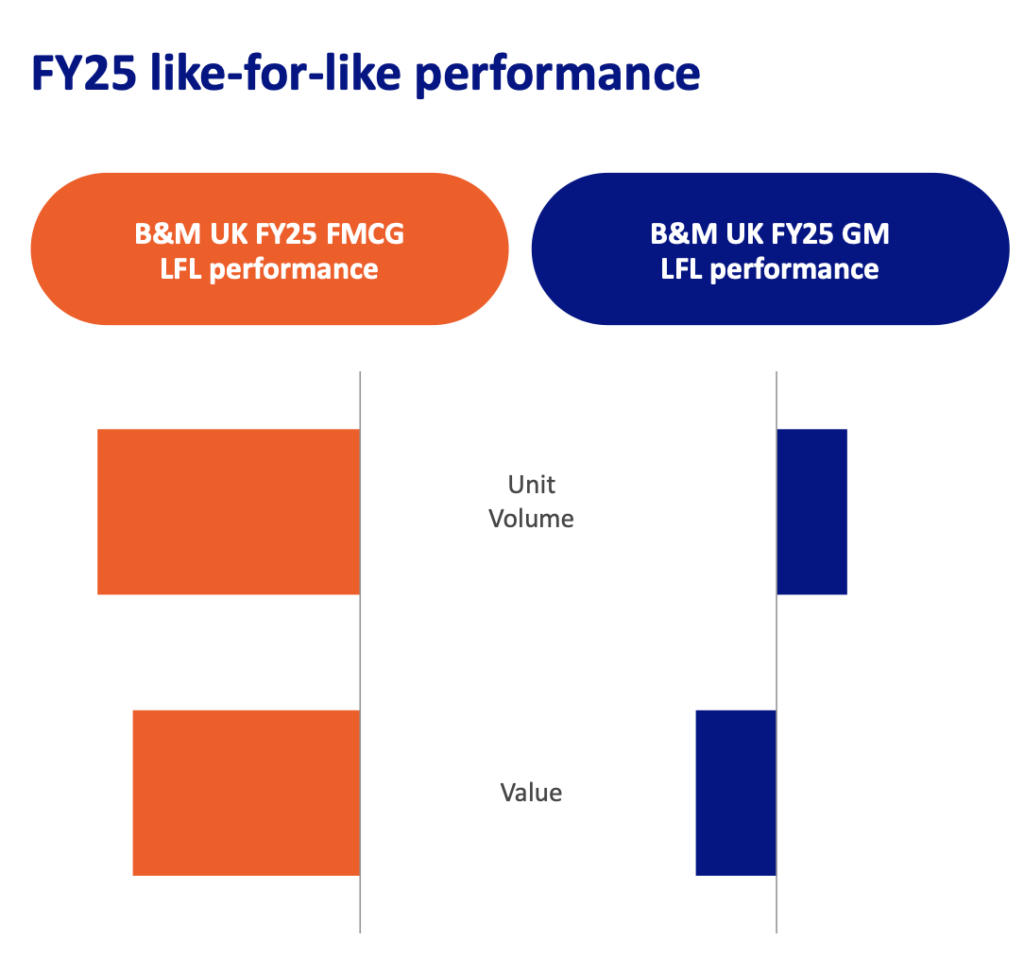

LFL declined in the UK by -3.1% due to poor FMCG execution, and GM purchases value was offset by deflation in this area, but with an improvement in volume:

The company in 2025 presented some actions to improve the current LFL in FMCG and GM. After presenting the Q1 2026 sales update, LFL grew 1.1% (total 4.7%) (below expectations of 2%), but for me, it is a good result, and the management can still take actions to continue making improvements.

Another thing to note is that the company has a lot of purchases from General Merchandise. This implies that heavy purchases in this segment come during festive seasons.

Management

The architect of this company is Simon Arora, who retired from the company in 2021 after 17 years. Then Alex Russo entered as CEO, but he retired in April 2025. I suppose the board requested his departure due to bad performance in meeting guidance each year.

Now the new CEO is Tjeerd Jegen. Before entering, he bought more than 500k GBP of his own money in B&M stocks. He wants to be aligned with shareholders.

He presented the latest Q1 2026 update, but of course he has been in the company for less than 1 month, so I am expecting new results.

Another important thing that I did not mention is that this company pays dividends every year. The company was originally formed in Luxembourg but redomiciled to be able to do a share buyback.

Continue with numbers…

Okay, we see that the company is easier to understand. It grows, pays dividends each year, is going to do a buyback, and comparables are easier to find. I prepared a small list:

I combined companies from the USA and Europe, but the variables are almost the same (I did not adjust the data; I just took it from Tikr).

The Debt to Equity ratio of B&M European Value is 60% (in line with the sector). The cost of capital after tax is 5.97% (pre-tax 6.97%), which is in line with other peers. ROIC is 14.05%, which is higher than the sector, and EBIT margin LTM is 10.16%, in line with the average (but the average should be ignored in this case due to the higher margin of Dollarama. The median of the sector is 7.69%, so it is higher than the median).

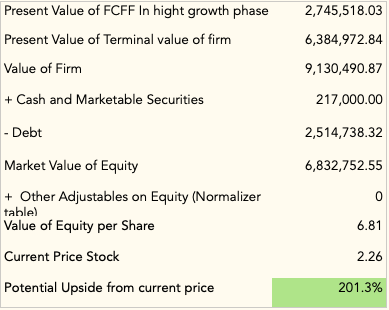

To value this company, I will start by using the fundamental growth (I shared spreadsheet at the end and looks at parameter on other scenarios):

A target price of 6,81 looks amazing! But the fundamental growth implies that growth impacts directly on operating profits, because each reinvestment gives us a return of 14% and contributes directly to operating profit. This can work for a lot of companies but not for B&M.

Let me explain in depth.

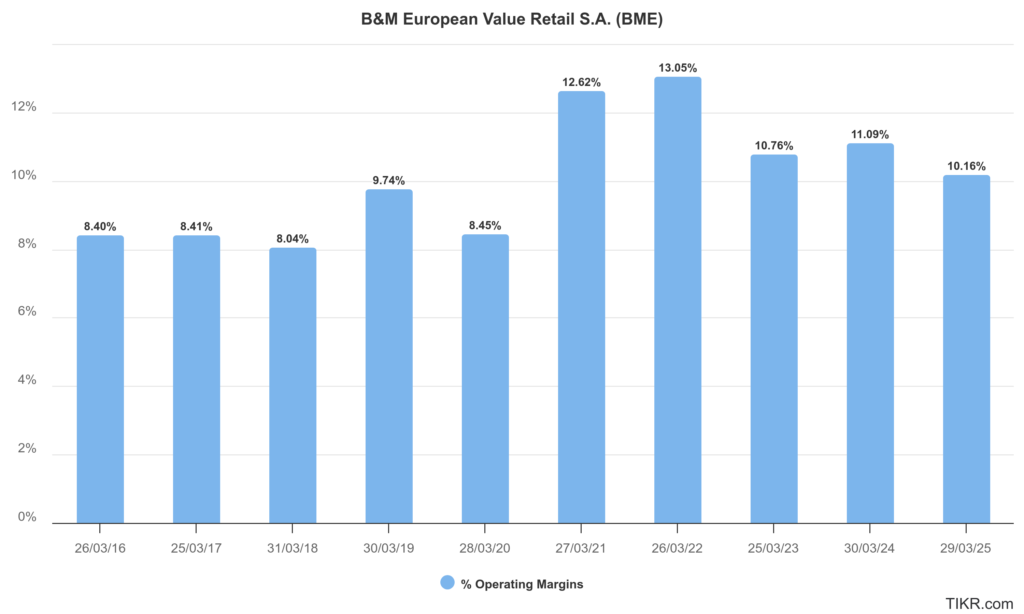

The current operating margins are at the 10.16% level. Before 2021, they were 8% on average. If we look at this graphic:

In 2021 and 2022, the company benefited from operating leverage due to panic purchases and gross margin improvement from a good strategy in GM. For this reason, I do not think this is sustainable in the future. Another reason is that the company expects to pay an additional £75 million next year in social security costs (including National Insurance, minimum wage, and other factors). For this reason, I expect the margins will rapidly drop to previous levels (maybe too conservative).

We must also expect additional competition, so the company must invest more in advertising and use a lot of pricing strategies in FMCG and GM, reducing gross margins.

With these margin expectations in mind, let’s adjust the valuation model accordingly and add different scenarios…

Back to growth, if we take the current number of stores and the target of 1200 in the UK, we get:

The calculation is simple: take the total number of current stores, divide by revenue, and we get an approximation of the revenue that each store generates. Then, we can get a simple growth number each year just from opening new stores, without lag, because each new store is profitable from day 1.

A weighted growth of 3.97% on new stores is too conservative. Each year, new stores add more than 5%, but B&M needs to do a lot of price actions. It can have deflation in some sectors (or inflation), so the total value of items can be affected.

Using the previous margin and revenue growth, I will build different scenarios.

Important clarifications for each scenario

- Working capital: 10% as a percentage of revenue. I took the average of similar companies.

- Growth in Stable Period: 2% – Average economy growth

- ROIC in Stable Period: The same as cost of capital in stable period. To be reasonable and not get an ultra-high terminal value that can affect valuation.

- Margins will decline quickly to 7% due to high competition and aggressive pricing actions.

Leases are included in debt. New leases each year are also included as CAPEX. It is important to do this, because the way this company grows with new stores implies adding new leases. This implies additional contractual obligations, additional right-of-use asset depreciation, and can heavily affect the simple Net-Capex calculation. To sum up, Net Capex Calculation = Purchase of Intangible Assets + Purchase of PPE + Addition of right-of-use assets – D&A.

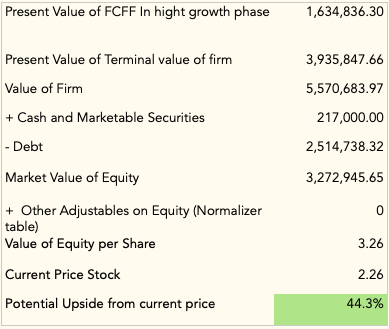

Scenario 1 – Base

This scenario only counts revenue from store growth, without any LFL growth.

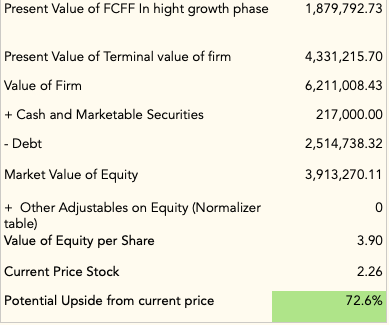

Scenario 2 – Mid

In this scenario, I count revenue growth from stores plus LFL growth of 1%.

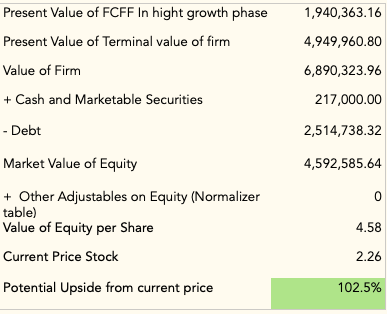

Scenario 3 – Optimistic

In this scenario, I count revenue growth from stores plus LFL growth of 1%, and margins decline to 8% and not 7%. This is because B&M does not take too many aggressive pricing actions but improves its advertising strategy, improves value to customers, and still continues to improve supply chain and cost efficiency.

Conclusion

In each scenario, you can see the complete models in this spreadsheet (some functions maybe doesn’t work because I exported from Apple Numbers). Feel free to copy it and add your own scenario.

I think this company has the potential to continue growing. Of course, we must follow the new CEO’s actions and pay special attention to margins—how they can be affected by competition or if the company takes aggressive actions that can hurt their free cash flow generation.

It is important to follow and adjust your position if some of the previous actions occur. But at the current stage, the company generates a lot of free cash flow and can continue generating it, pay dividends, and buy back shares. At current prices, this can give us good benefits, of course.