No investment advice, make your own research first

Havas has shared its results for the first half of 2025, which includes Q2. In this post, we will look at the key numbers and re-evaluate the company based on the latest data.

Revenue

Net revenue grew by 2.9% year-over-year to €1,346 million in the first half of 2025. Organic growth was 2.3%, and it sped up to 2.6% in the second quarter. However, foreign exchange headwinds hurt the results. I think these currency losses may continue this year because the euro is strong right now.

Margin

The adjusted EBIT margin improved to 10.7% from 10.2% in the first half of 2024. Adjusted EBIT reached €144 million, up 8.3%. This shows better efficiency in operations.

If we take the non-adjusted EBIT margins improved to 9,96% from 9,55%, reached 132 millions up 7,2%.

The company defines adjusted EBIT as EBIT minus restructuring costs and goodwill impairments.

We can use adjusted EBIT for a simple valuation. But remember, this ignores key costs for a company like Havas that grows through mergers and acquisitions (M&A). Restructuring costs matter because if the company is not good at combining businesses, these costs stay high. And of course if we are going to calculate

Debt

Gross debt was €430 million at the end of June 2025, while cash and equivalents were €351 million. The company has strong liquidity of €1,197 million. There are commitments like earn-outs, buy-outs, and buy-backs, which may total around €322 million this year based on earlier estimates. The added debt could help pay these.

Valuation

I will do some comparison with Publicis Groupe. I think this comparison is very useful. Publicis Groupe has much larger revenue (about 10 times bigger), better margins, and higher revenue growth and is mature than Havas. This revenue growth is important because many people would expect Havas to grow faster than Publicis Groupe, but that is not the case. Havas is growing at 2.5%-3%, while Publicis Groupe is growing at close to 5% and expects to keep that rate for at least the next few years. Of course, things are changing quickly in this sector. The introduction of AI could destroy current competitive advantages faster than we think or even harm the whole sector.

The current and expected growth of Havas is mediocre (2,5%). Its margins are relatively good when compared to similar companies (data from sources like Tikr and financial reports, using 2021-2024 because those are the main available data for Havas before 2025):

Analysts expect Havas to grow by about 2.5% on average for the next three years, and then about 1,5%. For The Interpublic Group of Companies (IPG), a drop in revenue is expected, with organic net revenue forecast to decrease by 1-2% in 2025. WPP Plc is the most affected company, with guidance for a 3-5% decline in like-for-like revenue less pass-through costs in 2025. Of course, these are analysts’ opinions, but it is worth seeing who the top performer is in this market (at least in Europe).

The advertising sector is mature and consolidated, with big global players and more fragmented regional ones. These smaller players will likely be bought by the largest companies because most growth comes from M&A.

All companies are making large investments in AI because it is the main driver in this sector now – if you do not invest, you could fail. All companies’ stocks are under pressure. So, it is important to note that the current market structure could change in a few years due to AI and more M&A.

Valuing Havas

Base Parameters

- Unlevered beta: 1 – The company lacks of stock price latest five year and his competitors has a Unlevered Beta of ~1.

- Levered Beta: 1,224 (if we took latest balance sheet Debt to Equity ratio of 32%)

- Marginal Tax Rate: 30%

- Cost of Equity: 10,18%

- After Tax cost of Debt: 3,01%

- Cost of Capital after tax: 7,83%

- ROC: 11,36%

- Reinvestment Rate: 42,33%

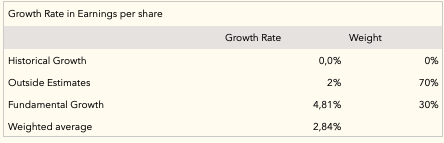

- Fundamental Growth: 4,81%

- Risk Free Rate: 3,35% (Netherland 10Y bond)

I am using last twelve months (LTM) data from the latest report and unadjusted EBIT to calculate Return on Capital (ROC). This is because if I want to calculate a correct ROC using adjusted EBIT, I also need to adjust the equity by removing impairments and restructuring costs. Otherwise, the ROC will be artificially higher.

In CAPEX, I include acquisitions, purchases PP&E, and intangibles. I do not capitalize R&D because I only have data from 2023 and 2024. In a note from the 2024 full-year report, the amounts are almost the same, so it is not necessary to capitalize.

The company has a commitment to invest 400 million euros in Converged.AI through 2027. I do not see high expenditures in 2024 or the first half of 2025 in CAPEX or R&D. This makes me think the company has not started investing yet. So, I will add 133 million to CAPEX in 2026 – 2027 – 2028. Just to be reasonable that will not be available to allocate all money in two years and maybe the project extend more time.

For the net change in working capital, to simplify, I set it to 0 for the next years. This avoids affecting the free cash flow to the firm too much (positive or negative). In some years, the company will have positive working capital (probably during stable growth), and in other years, not.

At the end of the valuation, I removed from equity some commitment that the company has: Earn-out & Buy-out for 289 millions and off balance-sheet obligations for 237 millions. All of them brought to present value.

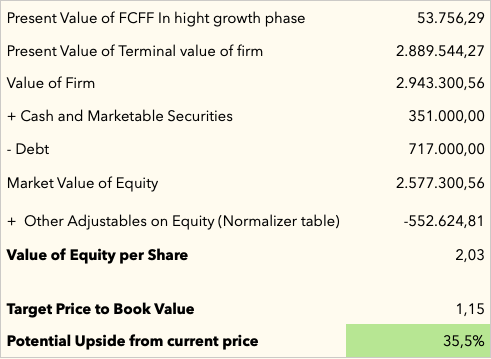

First Scenario – Highly probable

The fundamental growth shows a potential increase of 4.81% if the company reaches a ROIC of 11.36% in future investments. This is hard, but the company grew close to 3% in the first half of this year. In this scenario, we use the following growth table:

The outside estimation is the company’s guidance for organic growth through 2028. I think this is highly achievable and makes sense: it is less than inflation and close to GDP growth, nothing special. For this reason, I give it 70% weight.

The other 30% comes from possible M&A, which gives a weighted average growth of 2.84%.

Can AI add to revenue? No, I think not. AI will not directly help the company’s revenue but will improve operating margins.

This revenue growth period will be 3 years (2026-2027-2028). Then, the company will have stable growth of 1.5% (based on analyst estimates).

Margins improve from 11.15% to 12.5% unadjusted in 3 years. I think this is easy for the company and matches management targets (13%-14% adjusted). In this scenario, AI does not affect margins much, but it will help reach the 1.45% margin gain easily and meet management goals.

In the stable growth period, the debt-to-equity ratio goes to 20%. The company returns to its previous level by reducing debt. Beta goes to 1 like a mature company, giving a cost of capital of 7.74%.

The ROIC in stable growth equals the cost of capital to avoid destroying value. The company does not create value, but it does not destroy it either.

I think this scenario is too basic and average for the company. We are making really bad assumptions:

- The company’s investment in AI is completely useless. It does not improve much.

- The company grows less than target inflation.

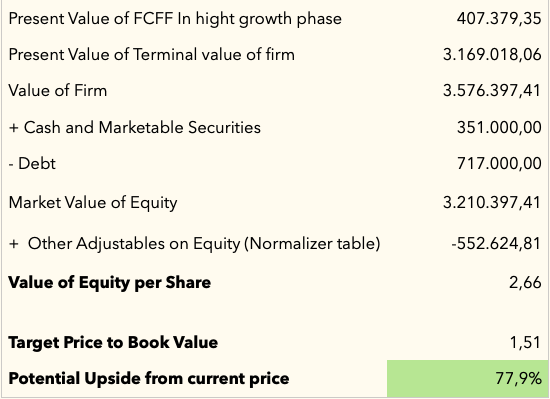

Second Scenario – Optimist

In this scenario, we use the following assumptions (the rest are from the previous scenario):

- Stable growth of 2% (target inflation rate)

- Margins improve to 15%, similar to Publicis Groupe by cost savings.

- High growth period of 5 years

In this case, the company gets strong operating leverage thanks to high adoption of AI, which can potentially provide big benefits.

Conclusion

In any case, I assume that Havas does not gain a higher market share than it has now. In the first scenario, the company is losing market share. It has no power to renegotiate prices, and at some point in the future, it will be acquired or fail.

The second scenario has high uncertainty (and is less probable). We should not use it as a target for the company because we do not know how well it will adopt AI. It is impossible to predict. For this reason, we must watch developments to decide if we add more shares to our position or not.

A target price-to-book value of 1x – 1.1x feels reasonable. Remember that Havas is trading below its book value while Publicis Groupe with higher quality and after a high drop of 24% YTD is trading at 2x book value.

Stocks options are partially covered by using diluted shares but it’s not a good practice and I’m not taking in account the compensation plan.

My position remains the same.