What does the company do?

It is a UK company that focuses on distributing and making packaging (mostly protective types).

It has two divisions. The manufacturing division supplies packaging to specific sectors like medical, diagnostics, aerospace, and automotive. This division makes up 20% of the revenue and has margins around 15%.

The distribution division makes up 80% of the revenue. It distributes protective packaging mainly for B2B e-commerce and industry. It uses several local distribution centers to make deliveries fast and cheap.

In 2003, the current CEO Peter Atkinson joined. In 2004, he started an action plan that included:

- Improving service

- Reducing costs

- Fixing relationships with suppliers

- Selling non-core assets

- Exiting non-strategic businesses

This plan led to the company pulling back its operations. Before, Macfarlane had a presence in the United States, Mexico, and other countries. Now, it focuses on the United Kingdom.

They also changed their focus to grow organically and through acquisitions. This takes advantage of the market, which is fragmented and mostly run by small companies.

They have already entered the German and Dutch markets with small acquisitions. So, the company is starting to expand again to other European countries.

Today, the company has a base of very large and stable customers. It does not depend too much on any one group of clients.

It is a UK company that focuses on distributing and making packaging (mostly protective types).

It has two divisions. The manufacturing division supplies packaging to specific sectors like medical, diagnostics, aerospace, and automotive. This division makes up 20% of the revenue and has margins around 15%.

The distribution division makes up 80% of the revenue. It distributes protective packaging mainly for B2B e-commerce and industry. It uses several local distribution centers to make deliveries fast and cheap.

In 2003, the current CEO Peter Atkinson joined. In 2004, he started an action plan that included:

- Improving service

- Reducing costs

- Fixing relationships with suppliers

- Selling non-core assets

- Exiting non-strategic businesses

This plan led to the company pulling back its operations. Before, Macfarlane had a presence in the United States, Mexico, and other countries. Now, it focuses on the United Kingdom.

They also changed their focus to grow organically and through acquisitions. This takes advantage of the market, which is fragmented and mostly run by small companies.

They have already entered the German and Dutch markets with small acquisitions. So, the company is starting to expand again to other European countries.

Today, the company has a base of very large and stable customers. It does not depend too much on any one group of clients.

Financial

The company has grown at a rate of 3.8% since 2004, when the transformation and strategy change began.

Operating margins went from breakeven in 2003 to 8.9% in 2024 over the same period (unadjusted).

Except for the last trailing year, when they fell to 7.1% due to salary increases and higher social security contributions in the UK.

In 2023 and 2024, the company saw revenue drop by 3.3% and 3.7%, but margins were not affected.

In 2023, this was due to weak demand in the UK and Ireland, falling selling prices, and a return to normal after COVID in e-commerce.

In 2024, there was price deflation, weak demand, and a big drop from new environmental rules on packaging.

Clearly, in both 2023 and 2024, without acquisitions, the revenue fall would have been much worse.

In the latest report (interim 2025), the company showed almost 0% growth in its Packaging division and 0.3% organic growth in Manufacturing. This means organic growth has likely hit its lowest point.

The Pietreavie acquisition added 83% growth (H1 2025 vs H1 2024) to the Manufacturing division.

Looking at the historical average for acquisitions on revenue (excluding years with no acquisitions), the annual rate is 3.32%. If we include years without acquisitions, it is 2.53%.

Macfarlane has a comfortable debt position, with the Net Debt/EBITDA ratio always below 2x.

For shareholder returns, the company pays dividends every year (about 40% payout ratio) and offers a current dividend yield of 4.30%.

Over the last 5 years, the stock price has only risen by 25%, with a strong increase in 2021-2022 during the COVID period due to more online orders. Then it was hit by the return to normal sales, but I think it has reached a bottom based on the 2025 report.

In the latest report, operating expenses rose sharply due to higher worker taxes, minimum wage increases, and rising raw material costs. However, compared to earlier years, the gross margin is much better than in 2019.

Management

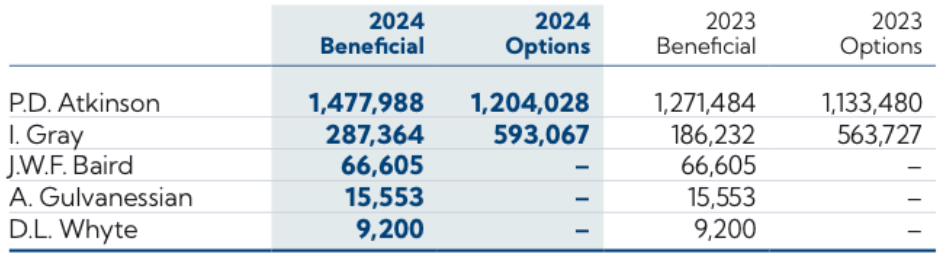

Let’s see, about the management in general, I can’t say much more than the CEO—who built the current Macfarlane—is still there. But I can’t help pointing out one thing that worries me: the CEO and the board (at least from the information I found) own few shares.

In fact, the CEO sold several of the shares he got from the company’s compensation plan on the open market.

In this table, we see that overall they own very few shares (especially for a CEO of a small-cap company with more than 20 years of experience who has obviously done a good job).

One positive thing: Directors and the CEO made buys in the last few weeks. Source.

Valuation

I made a Discounted Free Cash Flow to the Firm analysis, with three scenarios. You can download the complete excel here: